- LOGIN

- MemberShip

- 2026-07-22 05:43:22

- Varying performance levels of medical imaging AI companies

- by Hwang, byoung woo | translator Hong, Ji Yeon | 2026-05-26 15:21:32

Domestic medical imaging artificial intelligence (AI) companies reported varying performance in their first-quarter results, even as they posted losses.

While attention was previously focused on whether these companies could generate any sales during the initial stages of commercialization, the market is now asking "How do these companies make money?"

Consequently, the attention is on the Q1 2026 performance is not top-line sales rankings, but rather the specific channels through which sales is generated. Performance divergence among medical imaging AI companies is accelerating, depending on factors such as overseas commercialization channels, integration into domestic institutional healthcare frameworks, and volume-based recurring revenue streams.

Positive indicators in overseas·recurring revenue…Lunit·Coreline Soft differentiating factors

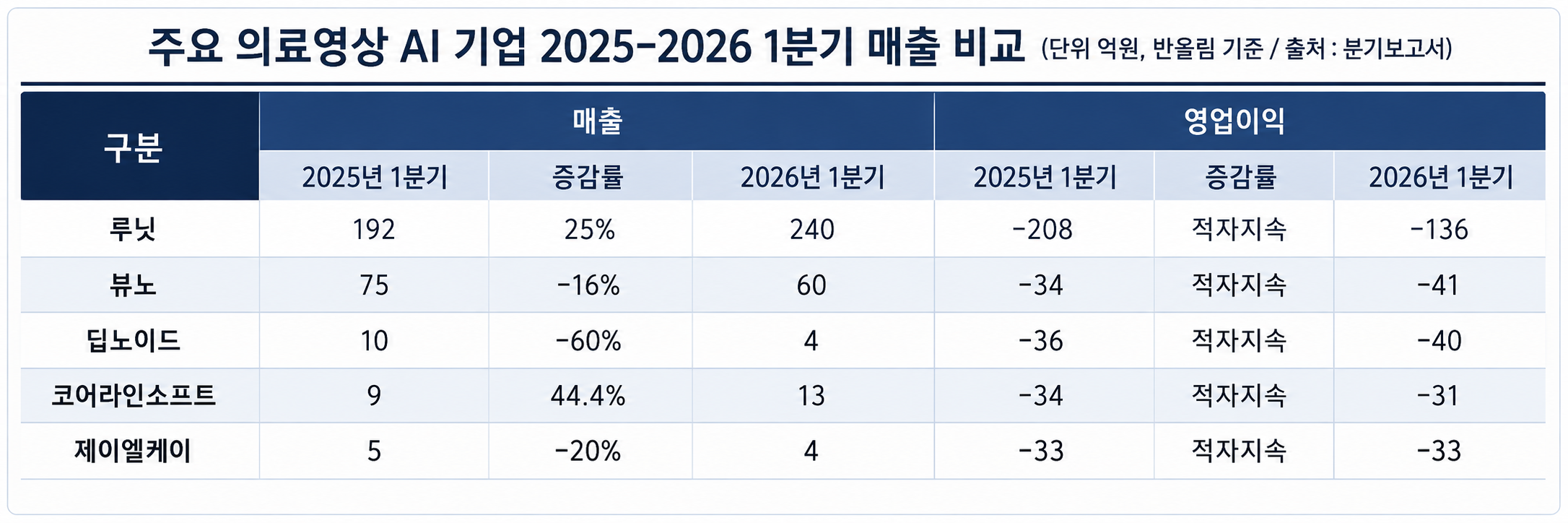

Lunit recorded revenue of KRW 24.0 billion for the first quarter of 2026, a 25% increase compared to the KRW 19.2 billion recorded in the same period last year. Concurrently, its operating loss narrowed from KRW 20.8 billion to KRW 13.6 billion, demonstrating increased revenue alongside a reduction in losses.

The most critical indicator in Lunit’s performance is its overseas revenue. According to the company's Q1 financial data, international sales reached KRW 23.2 billion, a 29% increase from KRW 17.9 billion in the prior-year period, accounting for a 97% of total revenue.

Domestic medical AI markets are highly susceptible to institutional and regulatory factors, such as New Medical Technology Assessments, non-reimbursement status, and reimbursement rates. Conversely, Lunit has successfully established a structure in which the vast majority of its quarterly revenue is secured through global distribution channels.

By business segment, cancer screening remains the primary growth driver. Software revenue from Lunit's cancer screening segment totaled KRW 21.3 billion in Q1, accounting for approximately 89% of total revenue.

Although its cancer treatment decision-support segment, which includes Lunit SCOPE, is emerging as a new growth vector, the core revenue generator as of Q1 2026 remains the cancer screening business, which includes diagnostic imaging assistance and breast cancer screening software.

However, challenges persist on the bottom line. While its operating loss narrowed, the company still posted a KRW 13.6 billion deficit in the first quarter. Although an improving trend in profitability has been confirmed, further revenue expansion and disciplined cost management are required to achieve a turnaround to operating profitability.

Coreline Soft, while not yet achieving Lunit's massive exterior performance, showed other positive indicators in its revenue structure.

Coreline Soft recorded consolidated revenue of KRW 1.3 billion in the first quarter of this year, representing an approximate 44% increase year-over-year.

Out of this total, overseas revenue amounted to approximately KRW 800 million, representing 62.4% of its overall business. This was the first time the company's international revenue share has exceeded 50%.

The expansion of its recurring revenue stream is also noteworthy. The company announced that the share of recurring revenue derived from volume-based utilization, term licenses, and software maintenance agreements reached 49.1% in Q1, climbing roughly 10 percentage points from 38.9% in the prior-year period.

Specifically, volume-based pay-per-use revenue surged by 319.7% year-over-year. This indicates that the business model of medical AI companies is successfully pivoting from one-off, on-premise deployments and perpetual license sales toward a framework dynamically tied to actual utilization rates and diagnostic screening traffic.

This structural shift is closely aligned with international national screening initiatives. According to Coreline Soft's documents, the company secured 11 new hospital contracts in Germany during Q1 alone, surpassing its entire annual total of 10 new contracts in Germany for the previous year within a single quarter.

Coinciding with Germany’s statutory health insurance reimbursement coverage for low-dose CT (LDCT) lung cancer screening, demand for AI-driven diagnostic reading, quality control, and longitudinal tracking systems is poised for further expansion.

Ultimately, Lunit leveraged international revenue to establish a quarterly baseline of over KRW 20 billion, while Coreline Soft signaled a clear structural pivot toward recurring revenue streams despite its smaller absolute volume. The former differentiated itself through scale, and the latter through its business model structure.

Vuno shows high reliance on DeepCARS…performance staggers due to regulatory variables

In the case of Vuno, the company had previously achieved record-high consolidated annual revenue of KRW 34.8 billion last year, growing 35% year-over-year, and successfully narrowed its operating loss by 60% down to KRW 4.9 billion through aggressive cost-optimization initiatives.

Performance was led by its flagship product, DeepCARS, an AI-driven cardiac arrest prediction medical device, which generated KRW 25.7 billion in revenue, representing an approximate 18% year-over-year increase.

However, its momentum slowed in the first quarter of 2026, with revenue dipping 16% quarter over quarter to KRW 6.0 billion.

The company explained that this temporary revenue fluctuation occurred as DeepCARS navigated the New Medical Technology Assessment process, coinciding with the expiration of its assessment deferral window.

Vuno’s challenge lies in the high concentration of its core revenue stream in domestic DeepCARS sales.

Although Vuno has designated the US commercial launch of DeepCARS as its top strategic priority, a fully realized revenue stream backed by US regulatory clearance and insurance reimbursement has not yet materialized. Consequently, Vuno's Q1 financial performance remained dependent on domestic DeepCARS sales and the progress of the domestic New Medical Technology Assessment procedures.

While market expansion is anticipated once the regulatory assessment process is finalized, establishing and diversifying commercial pipelines in global markets remains an urgent, ultimate objective.

Deepnoid·JLK, In a transitional phase prior to scaling revenue volume

Deepnoid generated only KRW 7.5 billion in annual revenue, falling significantly short of its previously guided revenue forecasts.

Deepnoid attributed this discrepancy to slower-than-expected expansion in medical AI adoption, delays in securing health insurance reimbursement pricing and international regulatory clearances, and intensifying competition from incumbent PACS (Picture Archiving and Communication System) vendors.

Furthermore, Deepnoid disclosed that it halted the standalone commercialization of DEEP:PHI, citing diminished differentiation for platform-type business models following the advent of generative AI.

Its revenue for the first quarter of 2026 amounted to approximately KRW 400 million. Even within this figure, the company relied heavily on its industrial AI division (roughly KRW 300 million) rather than its core medical AI segment (which brought in just KRW 57.75 million).

As operating deficits widened due to increased fixed costs associated with R&D scaling and expert talent acquisition, the company’s top priority has shifted to proving the self-sustainability of its medical division. This hinges on successfully anchoring its cerebral aneurysm solution, "DEEP:NEURO," within the domestic non-reimbursement market.

JLK is actively driving market entry into the non-reimbursement sector for its pipeline expansion, including its large vessel occlusion (LVO) detection solution, "JLK-LVO", starting with the current non-reimbursement prescriptions of its ischemic stroke solution, "JLK-DWI."

However, to overcome the limitations of a constrained domestic market, the company is committing substantial capital to establishing international commercial networks via its wholly owned subsidiaries in the United States (JLK USA INC.) and Japan (JLK Japan, Inc.).

Both JLK USA and JLK Japan reported zero revenue in the first quarter, posting net losses of approximately KRW 100 million each. Because these international subsidiaries have yet to generate meaningful top-line contributions, the company is currently in a wait-and-see window to determine whether these infrastructure investments will successfully translate into global financial performance.

A medical device industry employee stated, "With digital health companies that have secured insurance reimbursement pricing recently reporting robust financial metrics, pressure to perform is intensifying for medical imaging AI firms as well. We have entered a stage where regulatory clearance or initial hospital adoption alone no longer satisfies market evaluation. The core mandate now is establishing a commercial architecture that translates into sustainable, predictable revenue."

-

- 0

댓글 운영방식은

댓글은 실명게재와 익명게재 방식이 있으며, 실명은 이름과 아이디가 노출됩니다. 익명은 필명으로 등록 가능하며, 대댓글은 익명으로 등록 가능합니다.

댓글 노출방식은

댓글 명예자문위원(팜-코니언-필기모양 아이콘)으로 위촉된 데일리팜 회원의 댓글은 ‘게시판형 보기’와 ’펼쳐보기형’ 리스트에서 항상 최상단에 노출됩니다. 새로운 댓글을 올리는 일반회원은 ‘게시판형’과 ‘펼쳐보기형’ 모두 팜코니언 회원이 쓴 댓글의 하단에 실시간 노출됩니다.

댓글의 삭제 기준은

다음의 경우 사전 통보없이 삭제하고 아이디 이용정지 또는 영구 가입제한이 될 수도 있습니다.

-

저작권·인격권 등 타인의 권리를 침해하는 경우

상용 프로그램의 등록과 게재, 배포를 안내하는 게시물

타인 또는 제3자의 저작권 및 기타 권리를 침해한 내용을 담은 게시물

-

근거 없는 비방·명예를 훼손하는 게시물

특정 이용자 및 개인에 대한 인신 공격적인 내용의 글 및 직접적인 욕설이 사용된 경우

특정 지역 및 종교간의 감정대립을 조장하는 내용

사실 확인이 안된 소문을 유포 시키는 경우

욕설과 비어, 속어를 담은 내용

정당법 및 공직선거법, 관계 법령에 저촉되는 경우(선관위 요청 시 즉시 삭제)

특정 지역이나 단체를 비하하는 경우

특정인의 명예를 훼손하여 해당인이 삭제를 요청하는 경우

특정인의 개인정보(주민등록번호, 전화, 상세주소 등)를 무단으로 게시하는 경우

타인의 ID 혹은 닉네임을 도용하는 경우

-

게시판 특성상 제한되는 내용

서비스 주제와 맞지 않는 내용의 글을 게재한 경우

동일 내용의 연속 게재 및 여러 기사에 중복 게재한 경우

부분적으로 변경하여 반복 게재하는 경우도 포함

제목과 관련 없는 내용의 게시물, 제목과 본문이 무관한 경우

돈벌기 및 직·간접 상업적 목적의 내용이 포함된 게시물

게시물 읽기 유도 등을 위해 내용과 무관한 제목을 사용한 경우

-

수사기관 등의 공식적인 요청이 있는 경우

-

기타사항

각 서비스의 필요성에 따라 미리 공지한 경우

기타 법률에 저촉되는 정보 게재를 목적으로 할 경우

기타 원만한 운영을 위해 운영자가 필요하다고 판단되는 내용

-

사실 관계 확인 후 삭제

저작권자로부터 허락받지 않은 내용을 무단 게재, 복제, 배포하는 경우

타인의 초상권을 침해하거나 개인정보를 유출하는 경우

당사에 제공한 이용자의 정보가 허위인 경우 (타인의 ID, 비밀번호 도용 등)

※이상의 내용중 일부 사항에 적용될 경우 이용약관 및 관련 법률에 의해 제재를 받으실 수도 있으며, 민·형사상 처벌을 받을 수도 있습니다.

※위에 명시되지 않은 내용이더라도 불법적인 내용으로 판단되거나 데일리팜 서비스에 바람직하지 않다고 판단되는 경우는 선 조치 이후 본 관리 기준을 수정 공시하겠습니다.

※기타 문의 사항은 데일리팜 운영자에게 연락주십시오. 메일 주소는 dailypharm@dailypharm.com입니다.

- Samoh Pharm’s expansion after Voxzogo reimb…orphan drug portfolio

- Reporter's view | Hwang, byoung woo

- “7-year Lorviqua data reshape trt strategy for ALK-positive lung cancer”

- Reporter's view | Son, Hyung Min